Publisher:

Bonnie King

CONTACT:

Newsroom@Salem-news.com

Advertising:

Adsales@Salem-news.com

~Truth~

~Justice~

~Peace~

TJP

Feb-05-2018 23:27

TweetFollow @OregonNews

TweetFollow @OregonNews

Speaking the Truth About Debt in Oregon

Salem-News.com BusinessOregon fares slightly better than other states, but still owes more than it generates.

Image: TruthinAccounting.org |

(SALEM, Ore.) - The State of Oregon is ranked at position #26 in terms of state debt in the United States. The total state debt as of 2015, per the US Census Bureau, was recorded at $13,061,182,000.

That translates into a state debt per person of $3,245. On a per capita basis, Oregon debt ranks at #24. Back in 2012, the state debt in Oregon was $86,678,268,000. That translated into a state debt per capita of $22,229, and the state had a per capita debt ranking of #8. Clearly there has been a dramatic improvement in Oregon. The US Debt Clock indicates that for the 4,133,560 population of Oregon, the debt to GDP ratio is 14.92%.

The debt per citizen – in real time in February 2018, is $8,594. The state’s GDP is $240.729 billion. Of that, debt amounts to $35.47 billion.

All of these figures make for interesting reading, but they don’t tell the story of what is causing debt levels to rise, or how Oregon residents can manage their debt more effectively.

A report by TruthinAccounting.org was released in April 2017. According to those figures, Oregon retirement debt now amounts to $424.2 million, or a burden of $300 per taxpayer.

The fast-facts breakdown of debt and income in Oregon indicates that there are $19.6 billion worth of assets to pay down $20.1 billion worth of debts. The shortfall amounts to $424.2 million.

Total assets valued at $47.444 billion, less capital assets of $18.886 billion, less restricted assets of $8.91 billion leaves $19.647 billion available to pay the bills. Unfortunately, that shortfall amounts to $300 per taxpayer.

The state currently has bonds valued at $12.148 billion, and liabilities of $9.432 billion. Debt relative to capital assets amounts to $5.916 billion, and unfunded pension benefits of $4.244 billion also need to be taken into consideration. Unfunded healthcare amounts to $161 million.

That’s how the bills are determined. Given that the taxpayer burden is less than $5,000, Oregon fares slightly better than other states, but still owes more than it generates.

What Impact Does All This Debt Have on Oregon Households?

Over time, Oregon has actually improved its credit ratings. Between 2004 – 2017, Oregon has improved from an AA- (2004) to an AA + (2017). In fact, the state has maintained that high grade rating since 2011.

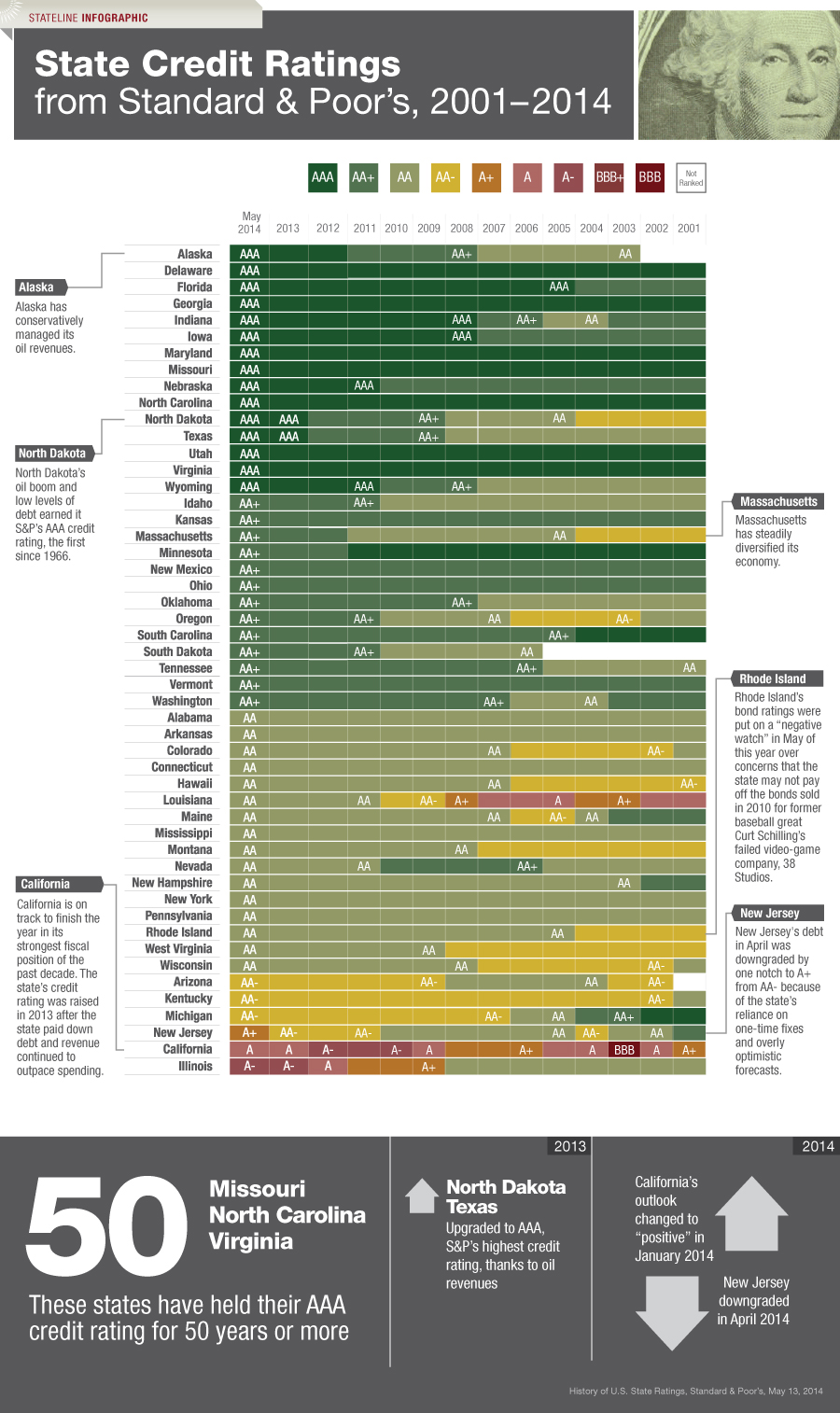

According to Pew Charitable Trusts, the top ranking states (AAA) include Alaska, Delaware, Florida, Georgia, Indiana, Iowa, Maryland, Missouri, Nebraska, North Carolina, North Dakota, Texas, Utah, Virginia, and Wyoming.

{kind=link}

Standard & Poor’s ratings indicate that Oregon is the middle of the road, but the best states include Virginia, North Carolina, and Missouri. These states have maintained their AAA rating for more than 5 decades. States with better ratings are associated with lower costs of credit, and large-scale investment of public projects.

Sound Advice for Bringing Down the Debt, Not the House

States that have overwhelming debt typically see lower levels of investment, which can affect the typical average household’s paycheck. There are many ways that debt impacts households, the most important of which is lower levels of disposable income.

This translates into lower savings rates, less money for a rainy day, and more paycheck to paycheck-style living. Experts routinely offer debt management advice to clients, notably in the form of understanding what creates debt, and how to take care of that debt.

Debt is divided up into good debt and bad debt. Bad debt is typically unsecured debt like credit card debts, personal loans, and the like. Good debt is typically considered mortgage debt. Student loan debt fits into both categories, but if you’re using your education, it should be considered an asset, not a liability.

Debt has grown dramatically since the 1950s, but today almost $13 trillion of household debt exists nationally, and approximately $3 trillion is credit card debt and non-mortgage debts.

Various methods are available to help alleviate this debt burden, such as reduced expenditure, credit counseling, debt consolidation loans, budgeting, and the use of cash and debit cards in lieu of credit cards.

Source(s): Data included in this report is derived from the state of Oregon's 2016 audited Comprehensive Annual Financial Report and retirement plans' actuarial reports; Salem-News.com Special Features Dept.

Articles for February 5, 2018 | Articles for February 6, 2018

Quick Links

DINING

Willamette UniversityGoudy Commons Cafe

Dine on the Queen

Willamette Queen Sternwheeler

MUST SEE SALEM

Oregon Capitol ToursCapitol History Gateway

Willamette River Ride

Willamette Queen Sternwheeler

Historic Home Tours:

Deepwood Museum

The Bush House

Gaiety Hollow Garden

AUCTIONS - APPRAISALS

Auction Masters & AppraisalsCONSTRUCTION SERVICES

Roofing and ContractingSheridan, Ore.

ONLINE SHOPPING

Special Occasion DressesAdvertise with Salem-News

Contact:AdSales@Salem-News.com

Salem-News.com:

Terms of Service | Privacy Policy

All comments and messages are approved by people and self promotional links or unacceptable comments are denied.

[Return to Top]

©2026 Salem-News.com. All opinions expressed in this article are those of the author and do not necessarily reflect those of Salem-News.com.